A Finance Guide to Revenue Recognition in SaaS: From First Principles to Real-World Complexity (and ARR!)

Revenue recognition in SaaS is deceptively tricky. At first glance, it’s just about spreading subscription revenue over the service term. But as your business grows—introducing multi-element contracts, usage-based pricing, upsells, and churn events—the complexity can escalate quickly! This guide covers the fundamentals for newcomers while diving into the operational and compliance nuances that experienced SaaS finance professionals must manage.

The Core Principle: Earned vs. Billed

In many traditional businesses, revenue is recognized at the point of sale or when a service is completed. In SaaS, however, the core rule is:

You recognize revenue when you’ve fulfilled your performance obligations, not when you invoice or get paid.

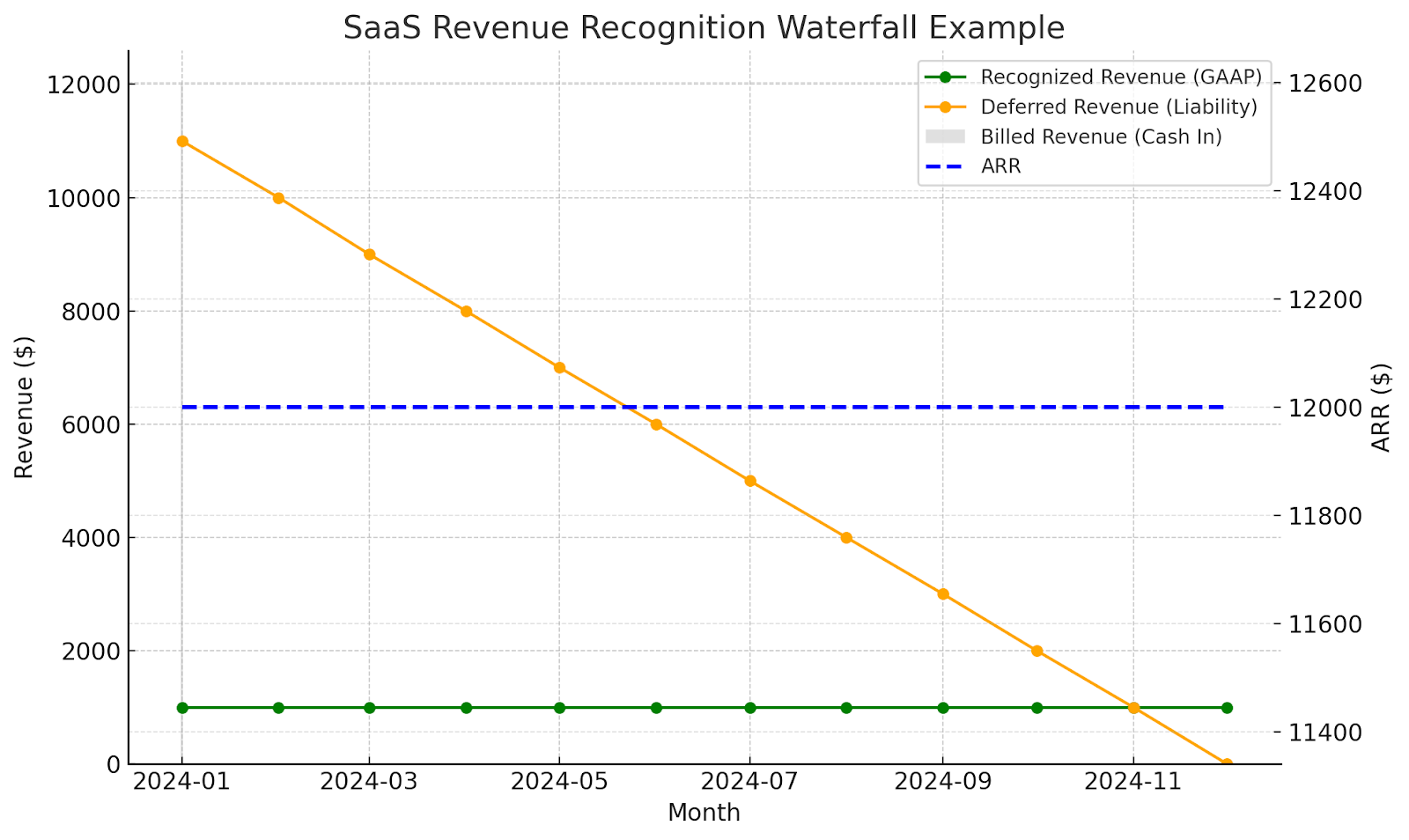

Example: The Simple Annual Subscription

Contract: $12,000 annual SaaS subscription signed Jan 1, billed upfront.

Cash flow: $12,000 hits the bank in January.

Revenue recognition: In January, you’ve delivered one month of service, so you recognize $1,000. The remaining $11,000 is deferred revenue—a liability—because you still owe 11 months of service.

ARR vs. Recognized Revenue: Two Metrics, Two Stories

Annual Recurring Revenue (ARR)

Definition: Forward-looking metric showing the annualized value of active recurring contracts.

Purpose: Forecasting growth, valuation modeling, sales performance tracking.

Example: That $12,000 annual contract = $12,000 ARR, regardless of when revenue is recognized.

GAAP Revenue (Recognized Revenue)

Definition: Backward-looking, audit-ready figure showing revenue earned in a specific period.

Purpose: Compliance, financial reporting, historical performance measurement.

Example: In Q1 of the same contract, recognized revenue is $3,000 ($1,000/month).

Key insight: ARR can spike instantly when you sign a big deal; recognized revenue accrues steadily over time. You need both to understand the health of the business—ARR for future potential, GAAP revenue for delivered performance.

Where Complexity Creeps In

The clean monthly allocation in our example is rare in a scaling SaaS business. Common complications include:

Mid-term upsells or downsells

Contract modifications require revisiting the allocation of transaction price and adjusting the revenue schedule.

ASC 606 outlines whether to treat it as a new contract or a modification of the existing one.

Multi-element arrangements

Bundling software subscriptions, professional services, and hardware means each element may have its own recognition pattern.

Requires calculating stand-alone selling prices (SSPs) for allocation.

Usage-based pricing

Recognized at the point of usage, not evenly over time. Often means running parallel recognition schedules for different revenue streams.

Churn and early terminations

May require reversing deferred revenue or accelerating recognition depending on contract and refund terms.

Multi-year deals with uneven billing

Creates deferred revenue that may span several fiscal years, requiring careful waterfall tracking.

Variable consideration

Discounts, rebates, or performance-based pricing need estimation and periodic re-evaluation under ASC 606 rules.

Operationalizing Revenue Recognition

Without automation, you’ll end up with complex spreadsheets that try to:

Track deferred revenue for every active contract.

Recalculate recognition schedules for upsells, renewals, and cancellations.

Keep GAAP compliance in the face of ever-changing contract terms.

Even a mid-sized SaaS company can have thousands of active recognition schedules running simultaneously. One incorrect formula can lead to material misstatements in financial reports.

Automating the Process: FinalStage.AI

FinalStage.AI streamlines revenue recognition by:

Compliance-first automation: Applies ASC 606/IFRS 15 rules to every contract in real time.

Dynamic handling of changes: Automatically adjusts recognition schedules for upsells, downsells, renewals, and churn.

Multi-element allocation: Calculates SSP splits and allocates transaction prices without manual intervention.

Clear visibility: Dashboards for deferred revenue, recognized revenue, ARR, and remaining performance obligations.

Result: Accurate, audit-ready numbers without spreadsheet firefighting, freeing your finance team to focus on strategic planning and growth initiatives.

Key Takeaways

Revenue recognition in SaaS is about earned value, not cash received.

ARR and GAAP revenue tell different parts of the same story.

Complexity grows fast—contract changes, multiple obligations, and usage-based elements multiply the moving parts.

Automation is essential at scale—not just for efficiency, but for compliance and accuracy.

Mastering these principles will make your financials rock-solid, your forecasts credible, and your board conversations a lot less stressful.